Fintechzoom Lucid Stock: Navigate the Future of Luxury EVs

In this article on Fintechzoom, we’ll analyze Lucid stock performance, financial health, competitive landscape, and growth prospects to help investors make informed decisions. Lucid Group (NASDAQ: LCID) has emerged as a prominent player in the rapidly growing electric vehicle (EV) industry.

Founded in 2007 and headquartered in Newark, California, Lucid Motors is focused on developing luxury EVs that combine high-performance, long-range, and cutting-edge technology. As investor interest in the EV sector soars, Lucid stock has been on a rollercoaster ride since the company went public in July 2021 through a merger with a special purpose acquisition company (SPAC).

About Lucid (NASDAQ: LCID)

Lucid Group, Inc. (NASDAQ: LCID) is a rapidly growing American electric vehicle manufacturer that has taken the automotive industry by storm. Founded in 2007 as Atieva, the company initially focused on developing battery technology for other vehicle manufacturers. However, in 2016, the company rebranded itself as Lucid Motors and shifted its focus to designing and manufacturing its own line of luxury electric vehicles.

Lucid’s mission is to inspire the adoption of sustainable energy by creating the most captivating electric vehicles centered around the human experience. The company’s first car, the Lucid Air, is a testament to this mission. The Lucid Air is a luxury sedan that boasts impressive performance, range, and efficiency, rivaling and even surpassing industry giants like Tesla.

One of Lucid’s key milestones was the completion of its state-of-the-art manufacturing facility in Casa Grande, Arizona. This facility dubbed the Lucid AMP-1 (Advanced Manufacturing Plant), has an initial capacity of 30,000 vehicles per year and is designed to be expandable to 400,000 vehicles per year. The company began production of the Lucid Air in September 2021, with deliveries commencing shortly after.

Lucid has also made significant strides in terms of funding and partnerships. In July 2021, the company went public through a merger with a special purpose acquisition company (SPAC) called Churchill Capital Corp IV, raising approximately $4.4 billion in the process. Additionally, Lucid has secured investments from prominent players such as the Saudi Arabian Public Investment Fund, which holds a substantial stake in the company.

Lucid Stock Performance

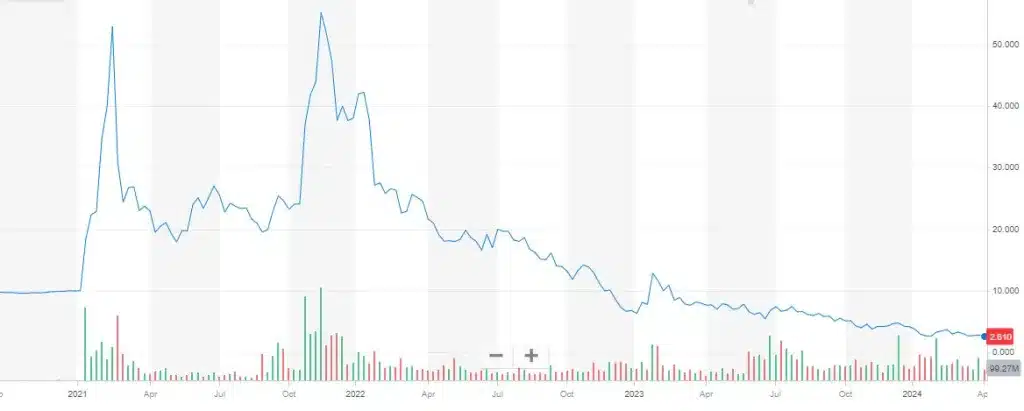

Lucid Group went public in July 2021 through a merger with a special purpose acquisition company (SPAC) called Churchill Capital Corp IV. The stock began trading on the Nasdaq under the ticker symbol “LCID” and initially surged, reaching an all-time high of $64.86 in February 2022.

However, Lucid’s stock price has been on a downward trajectory since then, influenced by various factors such as production challenges, supply chain issues, and the overall market sentiment towards growth stocks. In 2023, the stock hit an all-time low of $2.54 and has struggled to regain its earlier momentum.

Lucid’s stock performance has been closely tied to its ability to ramp up production and deliver vehicles to customers. The company has repeatedly revised its production guidance downward, which has led to investor concerns and stock price volatility. Additionally, the competitive landscape in the luxury EV market has intensified, with established players like Tesla and emerging rivals like Rivian vying for market share.

Lucid’s Financial Overview

As a relatively new entrant in the automotive industry, Lucid is still in the early stages of its growth trajectory and is not yet profitable. The company has been investing heavily in research and development, production capacity expansion, and marketing initiatives to establish itself in the luxury EV market.

In 2023, Lucid reported revenue of $595.3 million, a significant increase from the previous year but still falling short of analyst expectations. The company’s net losses amounted to over $2 billion in the first three quarters of 2023, primarily due to high cash burn rates associated with ramping up production.

Lucid’s balance sheet shows total assets of $8.51 billion and total liabilities of $3.66 billion, resulting in a total shareholder equity of $4.85 billion. The company has $3.86 billion in cash and cash equivalents, which provides some financial flexibility. However, Lucid’s debt-to-equity ratio stands at 42.7%, indicating a moderate level of financial leverage.

Lucid’s Production and Delivery Numbers

Lucid’s production and delivery numbers have been a key focus for investors, as they provide insights into the company’s operational performance and growth trajectory. In 2023, Lucid produced a total of 8,428 vehicles and delivered 6,001 vehicles to customers.

While these figures represent a significant improvement from the previous year, they fell short of Lucid’s initial guidance of producing 10,000 to 14,000 vehicles in 2023. The company faced challenges in ramping up production, including supply chain constraints and logistical issues.

In the fourth quarter of 2023, Lucid’s production and deliveries declined compared to the same period in the previous year. The company produced 2,391 vehicles (down 32% year-over-year) and delivered 1,734 vehicles (down 10% year-over-year). This slowdown has raised concerns among investors about Lucid’s ability to sustain its growth momentum.

Lucid’s Competiton Analysis

Lucid operates in the highly competitive luxury electric vehicle market, where it faces competition from established players like Tesla and emerging rivals like Rivian and Fisker. Lucid’s primary competitor is Tesla, which has dominated the EV market with its Model S sedan, a direct rival to the Lucid Air.

Compared to the Model S, the Lucid Air boasts a longer range, faster charging, and more spacious interior. The Air Dream Edition has an EPA-estimated range of 520 miles, surpassing the Model S Long Range’s 405 miles. Lucid’s Wunderbox technology enables bidirectional charging and high-speed charging up to 300 kW, allowing the Air to add 300 miles of range in just 20 minutes.

Lucid’s other competitive advantages include its proprietary electric powertrain technology, which delivers industry-leading efficiency and performance. The company’s in-house developed battery packs, motors, and power electronics contribute to the Air’s impressive range and power output.

However, Tesla has a significant head start in terms of brand recognition, production scale, and charging infrastructure. Tesla’s Supercharger network is widely available and provides a convenient charging solution for Tesla owners. Lucid is investing in its own charging network, Lucid Electric, but it will take time to match Tesla’s coverage.

Recent Developments and News

Lucid has made several notable announcements and developments in recent months. In August 2023, the company introduced the Lucid Air Sapphire, a high-performance version of the Air sedan with over 1,200 horsepower and a top speed of 205 mph. The Air Sapphire is positioned as a direct competitor to Tesla’s Model S Plaid and aims to attract performance-oriented buyers.

In November 2023, Lucid unveiled its second model, the Gravity, a luxury electric SUV built on the same platform as the Air. The Gravity is expected to enter production in 2024 and will compete with the Tesla Model X, Rivian R1S, and other premium electric SUVs.

Lucid has also announced plans to expand its production capacity and global presence. The company is constructing a second manufacturing facility in Saudi Arabia, which is expected to have an annual production capacity of 155,000 vehicles. Lucid has also opened new retail locations and service centers in key markets like Europe and the Middle East.

Fintechzoom Analysis on Lucid Stock

Analyst opinions on Lucid stock are mixed, with some expressing optimism about the company’s long-term prospects and others cautioning about near-term challenges. As of April 2024, the consensus analyst rating for LCID is a “Hold,” with 6 analysts recommending a “Buy,” 4 recommending a “Hold,” and 2 recommending a “Sell”.

The average 12-month price target for LCID is $15.50, representing a potential upside of 45% from the current stock price. However, price targets vary widely, ranging from a low of $5 to a high of $28, reflecting the uncertainty and divergent views among analysts.

Bulls argue that Lucid’s superior technology, brand positioning, and growth potential justify a higher valuation. They believe that as Lucid ramps up production and expands its product lineup, it will capture a significant share of the luxury EV market and achieve profitability.

Bears, on the other hand, point to Lucid’s production challenges, high cash burn rate, and intense competition as reasons for caution. They argue that Lucid’s current valuation is stretched and that the company may face difficulties in executing its ambitious growth plans.

Risks and Challenges

Investing in Lucid stock comes with several risks and challenges that potential investors should carefully consider. One of the primary risks is the execution risk associated with scaling up production. Lucid has faced difficulties in ramping up production of the Air sedan, and any further delays or setbacks could negatively impact the company’s financial performance and stock price.

Another challenge for Lucid is the intense competition in the EV market. While Lucid has a competitive product in the Air sedan, it faces stiff competition from established players like Tesla and emerging rivals like Rivian and Fisker. These companies are also vying for market share in the luxury EV segment, and Lucid will need to innovate and differentiate itself to maintain its competitive edge continuously.

Macroeconomic factors such as rising interest rates and inflation could also impact Lucid’s stock performance. Higher interest rates can make it more expensive for companies to borrow money, which could limit Lucid’s ability to invest in growth initiatives. Additionally, if inflation persists, it could erode the purchasing power of consumers and potentially dampen demand for luxury EVs.

Regulatory and policy risks are another factor to consider. While the Biden administration has been supportive of EVs, any changes in government policies or incentives could impact the demand for electric vehicles. Additionally, Lucid will need to navigate complex regulatory environments as it expands into new markets globally.

Long-term Growth Prospects

Despite the risks and challenges, Lucid’s long-term growth prospects remain compelling. The global market for electric vehicles is expected to grow significantly in the coming years, driven by increasing consumer demand, government support, and technological advancements. Lucid is well-positioned to capitalize on this growth, given its focus on the luxury EV segment and its innovative technology.

Lucid’s flagship product, the Air sedan, has received positive reviews for its impressive range, performance, and interior space. As the company ramps up production and brings new models to market, such as the Gravity SUV, it has the potential to capture a significant share of the luxury EV market.

In addition to its core vehicle business, Lucid has opportunities to expand into adjacent markets and services. The company’s proprietary battery and powertrain technology could be licensed to other manufacturers, providing an additional revenue stream. Lucid could also offer energy storage solutions for residential and commercial applications, leveraging its expertise in battery technology.

Furthermore, Lucid’s focus on in-house development of key components and software could give it a competitive advantage in terms of cost, performance, and innovation. As the company continues to invest in research and development, it has the potential to make technological breakthroughs that could further differentiate its products and services.

Frequently Asked Questions (F.A.Q)

Is Lucid a good stock to buy?

Whether Lucid is a good stock to buy depends on your investment goals, risk tolerance, and time horizon. While the company has strong growth potential, it also faces risks and challenges. It’s essential to conduct thorough research and consult with a financial advisor before making any investment decisions.

What are the risks of investing in Lucid stock?

Some of the key risks of investing in Lucid stock include execution risks related to scaling up production, intense competition in the EV market, macroeconomic factors like rising interest rates and inflation, and regulatory and policy risks.

How does Lucid compare to Tesla?

Lucid and Tesla are both premium EV manufacturers, but Lucid is focused on the luxury sedan market with its Air model, while Tesla offers a broader range of vehicles. Lucid’s Air sedan boasts a longer range and faster charging compared to Tesla’s Model S, but Tesla has a significant lead in terms of brand recognition, production scale, and charging infrastructure.

Conclusion

Lucid Motors stands at a critical juncture in the electric vehicle industry, characterized by rapid technological advancements and shifting market dynamics. The company’s innovative approach to EV design and its strategic financial partnerships have garnered attention, but it faces significant challenges in scaling production and achieving profitability. Investors considering Lucid stock must weigh these factors carefully, balancing the potential for high returns against the risks inherent in the volatile EV market.

![Fintechzoom Bitcoin Price Analysis and Predictions [2024]](https://thefintechzoom.com/wp-content/uploads/2024/04/Fintechzoom-Bitcoin-Price-768x432.webp)